Jet black (ideea is very interesting) started in 2018

“We’ve learned a lot through Jet black, including how customers respond to the ability of ordering by text as well as the type of items they purchase through texting,” said Scott Eckert, Senior Vice President.

As a learning experience for Walmart it seems all good.

Personally I appreciate the courage to run such an experiment, but Walmart can afford to do it anyway.

What did go wrong?

It seems a customer of Jetblack spent an average of 1500 $ per month, but the costs for Walmart amounted to $15,000 per year per member, as of last summer. Also, JB overlapped with Walmart’s own home delivery options, including its successful Walmart Grocery service, which could deliver the fresh food Jet black could not.

Around 300 employees in JB are going to be laid off soon.

Approval obtained from People’s Bank of China (PBoC) to begin formal preparation to set up a bank card clearing institution in China

MC are not the first US credit institution to require approval from PBoC. Also, Amex (American Express) had submitted the file in 2018. PayPal is targetting GoPay (PP are willing to pay for 70% of GoPay stakes).

Mastercard together with NetsUnion (both companies having set up a joint venture last year whereby NetsUnion is a clearing house for online payments whose stakeholders included PBOC) refiled this year its application as a joint venture called Mastercard NUCC Information Technology (Beijing) Co., Ltd. That application has now been approved.

According to the source below, it seems that the approval of MC (as well as of Amex – through with Amex’s Chinese partner LianLian Group – they both have a joint venture) are a part of the U.S.- China trade deal, which required Beijing to accept and review payments firms’ applications in a timely manner, which hadn’t happened before.

Anyway, they have competitors in Chinese market. China had 8.2 billion bank cards in circulation by the end of September 2019, 90% of them being debit cards. For example, local actors like WeChat Pay will fight to avoid losing market share.

Yet mobile payments in China are expected to grow 21.8% from 2017 to $96.73 trillion by 2023, and the total number of active mobile payment customers is expected to reach 956 million by 2023, up from 562 million in 2017.

Interesting to watch these evolutions: either China joining a western style of payment, or US companies will not succeed there. Will see.

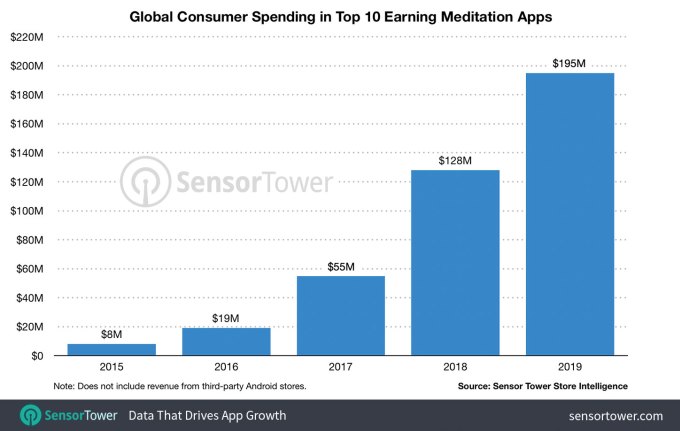

Those apps recorded $195M in 2019 – increasing by over 50% compared to previous year

Apparently, such evolution has been originating from millennials’ lifestyles, such persons chosing to marry later in life and delay having children; and because of that, it seems they allow themselves more time to remain self-focused, compared with their parents’ generation.

Also, internet acces had a more positive advantage for millenials when comparing to the previous generations: they have thus an easier access to information and therefore become better informed about welness and self-care.

Calm and Headspace (two mobile apps) registered (final figures not available though) $92 millions in 2019, and $56 millions respectivelly. Also, they have 24 millions new users in 2019 (Calm) and 13 millions (Headspace).

Next years I think millenials will determine more and more the market evolutions based on their interests, toward a direction or another. Will be interesting to watch these trends!

A business analyst need some business intelligence applications or tools (for example http://www.sas.com) and employ some methods to build a statistical model for the data he/she is analysing. But what if instead of laborious work to build a statistical model (even though SAS or other classical tools allow for this), a machine learning tool could help the statistician during this process and finally make his/her life easier?

A statistical model, if proven correct, will eventually anticipate consumer behaviour. These means a lot of opportunities for cross selling, inventory prediction (that will be prepared according to the model – see seasonalities, for example, that the statistical model will take into consideration in its prediction) and a bunch of good things will be anticipated.

Using business intelligence and analytics tools a statistician digs into data when building such a model. Someone said the other day that a company will build over a pre-defined period of time from 5 to 7 statistical models, out of which one of them will eventually work.

Pecan is for those who want to bring the power of machine learning to their data analysis, but lacks the skills to do it.

The Pecan AI tool includes a series of templates designed to answer common business questions divided into two main categories. The first is customer questions and the second is about business operations questions, i.e. related to things like risk.

There is also a third possibility: build your own template, but apparently this defeats the purpose (simplicity) because Pecan CEO Zohar Bronfman says that building your own is really for more advanced users.

The innovation started from the problem defined as much of the work involved in building machine learning models is about getting data in a form that the a machine learning algorithm can consume.

“The innovative thing about Pecan is that we do all of the data preparation and data, engineering and data processing, and [complete the] various technical steps [for you],” Bronfman explained.

Total raised by the startup so far: $15 million. The platform is builded since 2016 and Pecan has been working with beta customers for the last 18 months.

I like how AI is supposed to help human and make their life easier. This tool could be an example of such good “cooperation”.

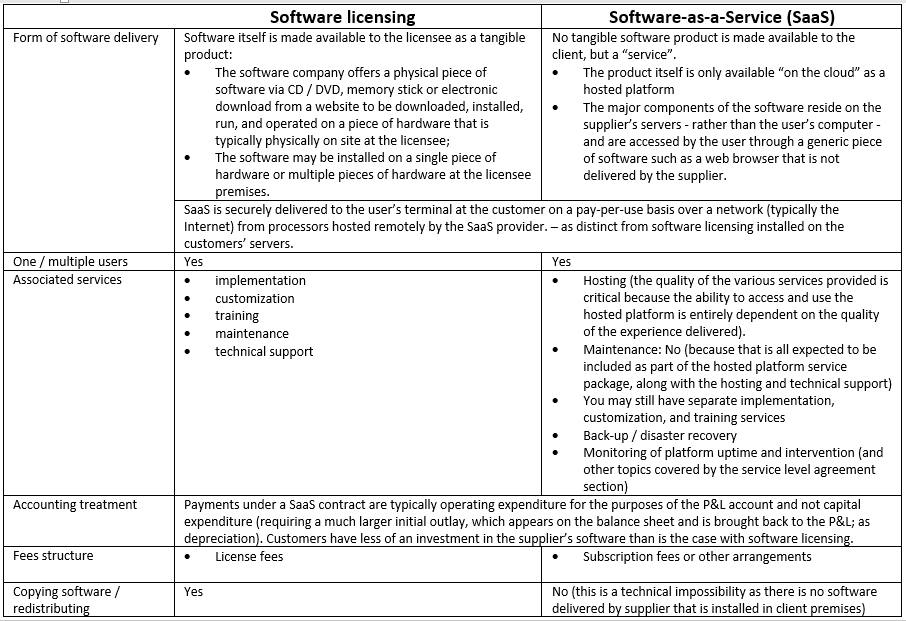

Cloud is more and more used to deliver IT related services under the form of software applications and systems

A comparison between Cloud software (SaaS) and classical Software licensing:

As a form of delivery of software, the difference is whether what is delivered is a tangible product or not. SaaS is not a tangible product (as compared to software licensed with deployment on client side including executable files than depend on client’s operating system, with the licensor wanting to control how many copies of software are distributed and all that stuff).

Multiple users are also possible with SaaS, I would say there is no limitation (except maybe the server capacity of Supplier to service thousands of users or so that could access SaaS concurently).

From the perspective of associated services, there is no maintainance, but still training and support is the case. Also, disaster recovery / business continuity, but this is no longer on client side, but in Supplier responsibility. This difference is important.

Another important topic remains a Service Level Agreement. This establishes a minimum level of availability of service that the Supplier must comply with as for the Client to be able to continue the work during its working hours. Important is also the network communication. It needs to be secure enough, as opposite to Software licensing whereby the software can work locally and is less exposed to Wild Web – and this is in case the business model does not imply links to other business partners (but very few cases, though, as nowdays we live in a connected world).

As far as accounting treatment is concerned, SaaS is different than software delivery under the form of some tangible product, because SaaS is rather an expenditure which goes on P&L, as compared to a tangible product such as software which goes on Balance Sheet of client (intangible assets) and only depreciation goes to P&L, but progressivelly during the lifetime of the delivered software product. There are pros and cons to each alternative from accounting view.

As far as payment is concerned, both software licensing and Saas could have various fees arrangements. For SaaS there is common the subscription fees structure or even fees per client transaction. Software licensing could also have various arrangements, but I don’t think a fee per transaction is usual as it might be applicable for SaaS (in rare cases, though).

Finally, there is no possibility to copy or redistribute software in case of SaaS, which it cuts off all stuff with copyright and control of licensor going to licensee premises and auditing about how many utilisations or users have using the undelying software product, if complying with number of licenses, etc.

Pros and Cons above should be carefully assessed when analysing the opportunity between the two alternatives.

Snyk innovation is to fit security in the development process.

In any development software company, during their development process, a separate security team takes the code offline and reviews it checking vulnerabilities in code (non necessarily aiming to find bugs). For example, they look into code and detect risks and recommends protecting against SQL injection, cross site scripting or other known weaknesses that developers are less focused on.

Snyk says this classic process can be speeded up, therefore they builds in security as part of the code commit.

Snyk offers an open-source tool to helps developers find open-source vulnerabilities when they commit their code to various open-source websites (GitHub, Bitbucket, GitLab) or any CI/CD (Continuous Integration / Continuous Development) tool. There is a community of 400,000 developers that practice this approach.

Snyk sells a container security product. Other income is generated from companies by taking advantage of a database with vulnerabilities they maintain. This is used in the open-source product.

The company claims revenue growth in 2019 (figures not public yet) four times than in 2018. Gaining in customer base are Google, Intuit, Nordstrom and Salesforce.

Previous financing: 2016 – 3millions $ (when started), then 2018 – 27 millions $ and latest 70 millions $

I see this as a cool idea, i.e. to automate building security into development. It seems Snyk are very good at this as long as they offer tools and a database with common vulnerabilities resulted out of the develpment process.

Visa is buying fintech Plaid (a company that it is now used by an estimated 25% of consumers in US, connecting users to 11,000 financial institutions). Amount of deal: $5.3 billion.

Plaid offers technology that allows consumers to link their bank accounts to its 2,600 fintech clients. Here there are included peer-to-peer (P2P) payments app Venmo, investing platform Acorns as well as stock-trading startup Robinhood. It is one of several players developing back-end infrastructure to enable fintechs to operate.

This deal size is within the rapid industry consolidation: providers look to M&A to avoid competition from upstarts in order to be better prepared for major shifts in the space, and to combat low margins.

Visa and Mastercard are known for high fees they charge for payments to companies for POS (Point Of Sale) devices connected as well as for settlement with banks. Due to kind of large banking network they have, they were kind of monopol.

However, PSD2 is opening the market of payments (at least in EU) to fintechs that can do payments in the name of clients, accessing bank accounts in their name.

The deal of Visa with Plaid is no exception: Visa sees Plaid as a tool that will help it in the next decade by improving fintech relationships and expanding Visa’s addressable market (according to CNBC).

But what’s in it for Plaid? Although they have such a significant traction in US, Visa can boost its operations outside US. Moreover, due to good reputation of Visa throughout banks, financial institutions will be more willing to allow data-sharing with Plaid.

We live interesting times, I keep an eye on these evolutions since PSD2 entered into force and banks (at least in EU) are to allow fintechs to create products for banks clients, accessing bank accounts, balances, transactions, all of these being for the benefit of final consumer.

French startup Lydia is raising a $45 million Series B round (€40 million). Tencent is leading the round.

Payments peer-ro-peer as their main business model now they shifted to a marketplace of financial products, such as borrowing (up to EUR 1000) in seconds, get a free credit when you open a bank account (cool!), home insurance (nice!) and utilities (electricity, gas and internet providers).

Lydia account can be connected to your bank account and debit card. It works with Google Pay, Samsung Pay, Apple Pay.

Looks to me like they are working using PSD2 standard since while ago (in Romania only in December 2019 the PSD2 law started to be in force).

Left column below shows how an enterprise (a company in general) gains value from innovation, achieve these objectives and then maintains a culture of innovation.

Right column: how to measure what is in the left column

I hope these hints will arm CIO/CTOs with tools that will allow them to consider filtering a few initiatives (existing more ore less in any company) that probably make more noise than they are well-grounded. These will establish a measuring system that will say more about what is to be pursued and what is not to.

What is important

to maintain an awareness of information technology and related service trends,

identify innovation opportunities,

plan how to benefit from innovation in relation to business needs.

First, it may be obvious to start with analysing what opportunities for business innovation or improvement can be created by emerging technologies, services or IT-enabled business innovation, as well as through existing established technologies and by business and IT process innovation.

influence strategic planning and enterprise architecture decisions.

What CIO / CTO can do

Except for no.2 that needs IT department’s help, the rest are more or less in the responsiblity of other functions within (any) company.

CIO could pursue the Board to look into no.1, have initiative together with HR (for no.3) and with the Board (and HR) for no.4.

No.5 is again a team work, including the CEO that might need to go systematic and encourage appropriate levels from the entire organisations in approaching customers, suppliers and business partners as to achieve this target of encouraging innovation in relation to third parties.